The AI buildup is being financed with your money

In 2026, the five largest cloud companies will spend $600–725 billion on infrastructure. About 75% — some $450 billion — goes into AI hardware that obsolesces fast: roughly 6 million Nvidia GPUs at ~$30,000 each.

No company can absorb a bet this size honestly. So the risk is being moved — across accounting estimates, off balance sheets, and into the retirement accounts of people who never agreed to hold it.

Then, in June, the demand side arrives: the three largest IPOs in history.

The supply side runs on three tricks

1. Depreciation. In November 2025, Michael Burry accused the hyperscalers — Meta, Amazon, Microsoft, Google, Oracle — of inflating profits through one estimate: how long a chip lasts.

- They depreciate GPUs over 5–6 years. Real economic life, given obsolescence, is 2–3.

- Stretching the schedule understates depreciation and overstates earnings — by an estimated $176 billion across 2026–2028.

- By 2028, Burry projects Oracle's profit overstated by ~27%, Meta's by ~21%.

"Understating depreciation by extending the useful life of assets artificially boosts earnings — one of the more common frauds of the modern era."

2. Circular financing. Nvidia sells chips, then invests in the firms that buy them — $40 billion+ in equity bets, ~$30B into OpenAI alone, which is on track to lose ~$14 billion in 2026. Analysts count $800 billion+ of these loops across the supply chain. A vendor that funds its own customers is telling you demand is softer than the revenue line says. The late-1990s telecom bubble booked growth the same way.

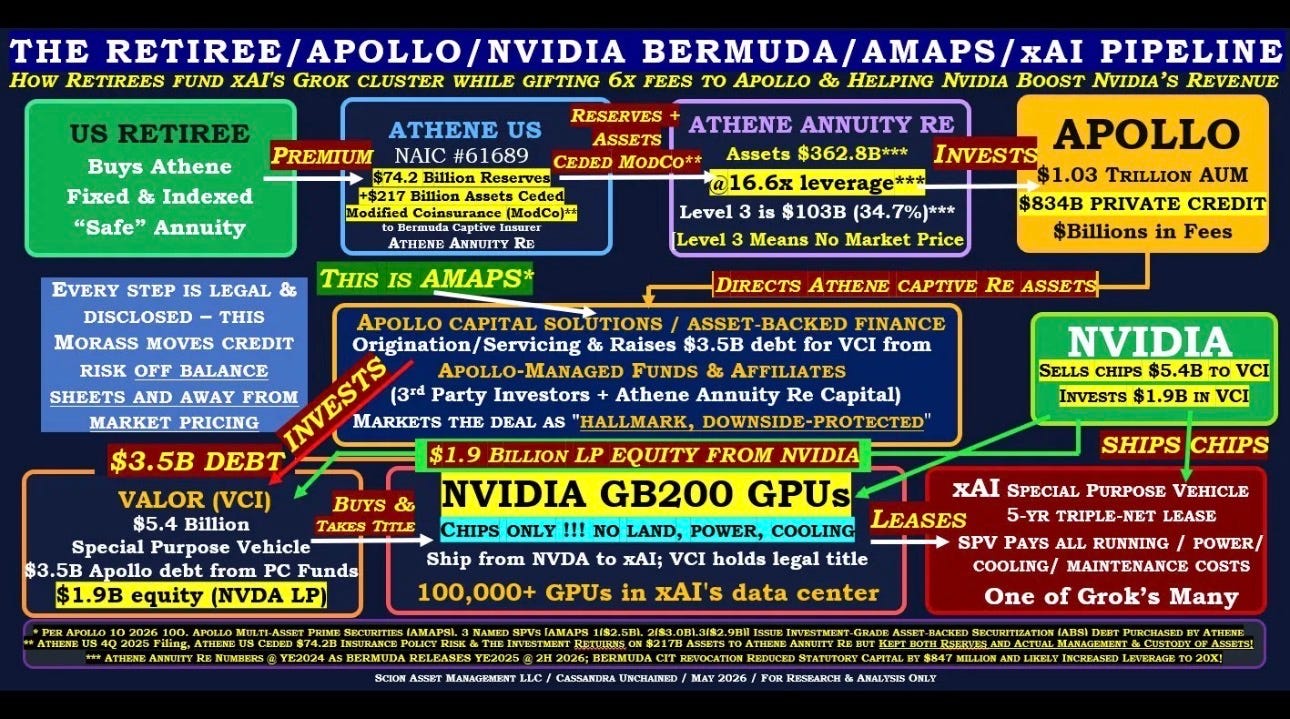

3. Off the books. The xAI deal (January 2026) is the cleanest specimen:

- Nvidia sells $5.4B of GPUs to Valor, an SPV — and puts $1.9B of its own equity into it as a partner.

- Apollo raises $3.5B of debt, marketed as "downside-protected."

- That debt is securitized and routed to Athene, Apollo's insurer, which sells "safe" annuities to American retirees.

- The GPUs stay off both Nvidia's and xAI's balance sheets via a triple-net lease.

Athene runs 16.6x leverage; $103B of its book is Level 3 — no observable market price; $217B sits in Bermuda captives, outside US oversight. Oracle, Meta, xAI and CoreWeave have moved $120B+ off balance sheet this way. A darker thesis circulates — that debt from Musk's Twitter buyout migrated through xAI into SpaceX before the IPO — but that chain is unverified. The verified part is enough: every step is legal and disclosed. That is the point. The risk was made boring enough that no one reads it.

The demand side arrives in June

- SpaceX — June 11, raising ~$75bn, trading June 12 on Nasdaq, valued at $1.75 trillion.

- Anthropic — filed draft IPO paperwork June 1.

- OpenAI — expected to file soon. The two labs are rumoured to seek ~$60bn each.

Together: ~$200bn raised, up to $4 trillion in new market value within months. The prior record raise was Saudi Aramco's $29bn in 2019. Steve Sosnik of Interactive Brokers calls the listings an "existential risk."

The forced bid: right fear, wrong denominator

To clear the path, the three index providers rewrote their rules weeks before the IPO:

| Benchmark | Old rule | New rule |

|---|---|---|

| S&P 500 | 12 months listed + 4 quarters of GAAP profit (since 2002) | both waived |

| Nasdaq-100 | 90 trading days | 15 |

| FTSE Russell | 90 days | 5 |

The profitability waiver matters most: SpaceX posted a $4.28bn GAAP loss last quarter. Under the old rules it could not have entered before 2027.

Now two numbers seem to contradict each other. They don't.

- The Economist: indices weight by free float. SpaceX is floating ~4% of itself, so its initial weight in the $69 trillion S&P 500 is about 0.1%. Your portfolio barely moves.

- Bloomberg Intelligence: S&P 500 funds must absorb 19% of SpaceX's float within six months; Russell 1000 and Nasdaq-100 funds, 24%.

Both are true. A 0.1% index weight is still tens of billions of dollars — chasing a float of only ~$75bn. Tiny slice of the index, enormous slice of the company, because passive money is now $30 trillion+ in 401(k)s and pensions. The funds don't choose; to track the index they must buy, selling Apple, Microsoft and Nvidia to fund it. And because every manager front-runs the rebalance, the buying starts before inclusion — lifting the price the funds will then pay.

The wealth transfer

Here is the mechanism in one sentence: forced buyers come in at IPO valuations, and locked-up insiders sell into them months later.

SpaceX insiders are barred from selling at first. After the Q1 report (~August) they can offload 20% of their stakes — another 10% if the stock trades 30% above its IPO price. Musk's ~half, carrying outsize voting rights, is locked for 366 days. Captive passive demand on one side, sellers released on a timer on the other. Wealth flows from pension funds to early investors, on schedule.

Why your fund still won't blow up on day one — and what bites later

The portfolio shock is small. The slow risks are not:

- Post-IPO drift. Jay Ritter's data on IPOs from 1980–2024: the average new stock returned 20 points less than the market over three years. Above 40x revenue: 58 points less. SpaceX would open above 90x revenue.

- Peak signal. Blockbuster IPOs cluster at market tops. The 2020–21 surge preceded a bear market; the late-1990s and pre-2008 booms preceded bigger slumps.

- Concentration. The ten biggest AI-linked firms are already 40% of the S&P 500. Bad news for SpaceX alone is survivable; bad news for AI is not. Equal-weight funds hedge it — but holding one now means betting against the market, the opposite of passive investing.

The capital diet

The deepest shift is structural. For a decade capital was abundant and shares were scarce: tech giants generated so much cash they bought back stock while workers poured savings in. Scarcity drove prices up.

That is reversing. The giants are halting buybacks to fund AI, tapping the bond market, and — through the giga-IPOs — issuing shares rather than retiring them. The supply of stock is rising just as the buyers' own jobs face automation. Victor Haghani of Elm Wealth calls what's coming a capital diet.

Investors will go crazy for the giga-IPOs. The indigestion comes later (maybe).